IRS Announces $500 Carry‐Over Provision for Health FSA Plans!

By Nathan Carlson President, 24HourFlex.com Nathan@24hourflex.com

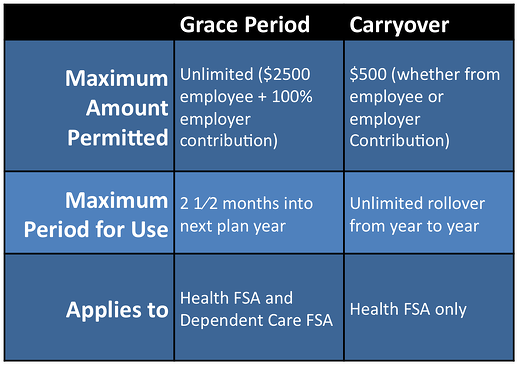

On October 31, 2013 the IRS announced that health FSAs can allow up to $500 of unused amounts at the end of the plan year to roll forward to the following plan year(s). This new carry‐over option is an alternative to the current IRS Grace period and does not affect the maximum health FSA cap of $2,500. To take advantage of this new carry‐over provision, the company’s Cafeteria Plan Document must be amended in a timely manner.

Example 1:

John chooses to contribute $1,000 to his company’s Medical FSA for 2014, a Cafeteria Plan that does not have the IRS Grace period and has elected to adopt the new IRS carryover provisions. This Cafeteria Plan also has a 90day run out period that allows participants until 3/31 of the following year to submit for reimbursement expenses for services rendered during the plan year. As of 12/31/2014, John still has $800 in his health FSA. Prior to 3/31/2015, John submits $300 of 2014 medical expenses for reimbursement, leaving $500 still unused as of 4/1/2015. This unused amount of $500 can roll forward and be spent on expenses incurred at any time during 2015 in addition to John’s 2015 health FSA funds. Assuming that John elected to enroll in 2015 in the health FSA for $1,000, John would actually have $1,500 to spend in 2015.

Which Cafeteria Plans can adopt this new Carry‐over provision?

Any Cafeteria Plan with a health FSA can adopt a Carry‐over provision if the plan does not contain the IRS Grace period. The plan cannot have both the IRS Grace period and a Carry‐over provision.i

When can the new Carry‐over provision be adopted?

Generally, the new Carry‐over provision must be adopted (via an amendment to the Cafeteria Plan Document), and any Grace Period language removed, by the end of

the plan year for which they are effective. However, for plan years beginning in 2013, the Carry over provisions must be adopted by the end of the 2014 plan year. In this case, the Grace Period language must still be removed by the end of the 2013 plan year.

What is the difference between the IRS Grace period and the new IRS Carry‐ over provision?

Essentially, the existing IRS Grace period allows any unused amount to be carried forward into the next year and spent within 21⁄2 months. However, after the Grace period and the run‐out period have expired, any unused funds are forfeited.

In contrast, health FSA plans containing the new IRS Carry‐over provision can allow up to $500 to be carried forward indefinitely until it is spent regardless of whether or not the employee continues to participate in the company’s health FSA.

It is important to note that funds rolled forward via the IRS Grace period or the IRS Carry‐over provision do not reduce or affect the $2,500 maximum cap on the health FSA.

Example 2:

Sue participates in her company’s health FSA that has the 21⁄2 IRS Grace period. For 2014, her annual health FSA election is $2,500. As of 12/31/2014 Sue has not incurred any medical expenses. Sue reenrolls in the health FSA for $2,500 for 2015. In February of 2015 Sue incurs $5,000 of eligible medical expenses, $2,500 is reimbursed from her unused 2014 funds and $2,500 from her 2015 election.

Example 3:

Assume the same facts as in Example 2 except that Sue’s company’s health FSA has the IRS Carryover provision rather than the IRS Grace period. Since only

$500 of Sue’s unused 2014 funds can roll forward to 2015, Sue will forfeit $2,000.

How does the presence of health FSA Carry‐over funds affect one’s HSA eligibility?

A full‐flex, health FSA is “impermissible coverage” when determining one’s HSA eligibility. In other words, one cannot contribute to an HSA if benefits are available under a health FSA. Therefore, an employee must exhaust his full‐flex, health FSA benefits if he intends to fund an HSA.

Example 4:

Joe participates in his company’s calendaryear fullflex, health FSA that contains the IRS Grace period. On 12/31/2013 Joe still has $100 in his health FSA account. Joe does not enroll in the health FSA for 2014 and spends his leftover 2013 funds in January of 2014. Per IRS guidance, Joe is ineligible to make a HSA contribution until April 1, 2014, the first day of the month following the IRS 21⁄2 month grace period.

Example 5:

Jim participates in his company’s fullflex, health FSA that contains the IRS Carryover provision. On 12/31/2013, Jim still has $100 in his health FSA account. Jim does not enroll in his company’s health FSA in 2014. So long as Jim has any money in his fullflex, health FSA account, he has “impermissible coverage” and is not allowed to make an HSA contribution. Jim will be able to make a HSA contribution on the first day of the month following the depletion of his health FSA, assuming that Jim is otherwise eligible to make an HSA contribution.

According to our legal counsel, this issue perhaps can be resolved if the Cafeteria Plan Document contains language that automatically transforms a full‐flex, health FSA into a limited‐purpose, health FSA upon the employee’s enrollment in a High Deductible Health Plan.

Will terminated employees have a COBRA election with respect to any unused health FSA funds that exist by virtue of a Carry‐over provision?

If the employer is otherwise subject to COBRA, a COBRA election must be granted for these unused funds.

Does the new Carry‐over provision apply to Dependent Care FSAs?

No, the new Carry‐over provision only applies to Health FSAs. On the other hand, the IRS 21⁄2 month Grace period can apply to health and/or dependent care FSAs.

Will 24HourFlex be administering health FSA plans containing the new Carry‐ over option?

Yes, the 24HourFlex system is presently capable of administering this new feature.

What is the process for adding the new Carry‐over provision?

- Decide the effective date for adding the Carry‐over provision.

- Notify your Client Relationship Manager at 24HourFlex of your decision to

- add the Carry‐over provision and the effective date of that decision—the plan

- year beginning in 2013 or 2014.

- If your Cafeteria Plan presently contains the 21⁄2 month IRS Grace Period,

- instruct 24HourFlex to remove this provision.

- Notify your employees in writing of the changes to the Cafeteria Plan.

(24HourFlex is developing a communication tool you can use).

To learn more and discuss with an expert, click here.

i The IRS Grace period allows plan participants 21⁄2 months after the end of the plan year to incur expenses. For example, a calendar‐year plan with the IRS Grace period would allow participants to incur health and/or daycare expenses up until 3/15 of the following year. The IRS Grace period differs from a run‐out period. A run‐out period allows plan participants an amount of time after the end of the plan year (i.e., 90 days) to submit expenses; however, these expenses must have been incurred during the plan year. Often Cafeteria plans contain both a Grace period of 21⁄2 months and a run‐out period of 90 days after the end of the plan year. Such a structure gives plan participants 15 days after the end of the 21⁄2 month Grace period to submit expenses for reimbursement, providing these expenses were incurred during the 141⁄2 month period (the normal 12 month plan year plus the 21⁄2 month IRS Grace period).